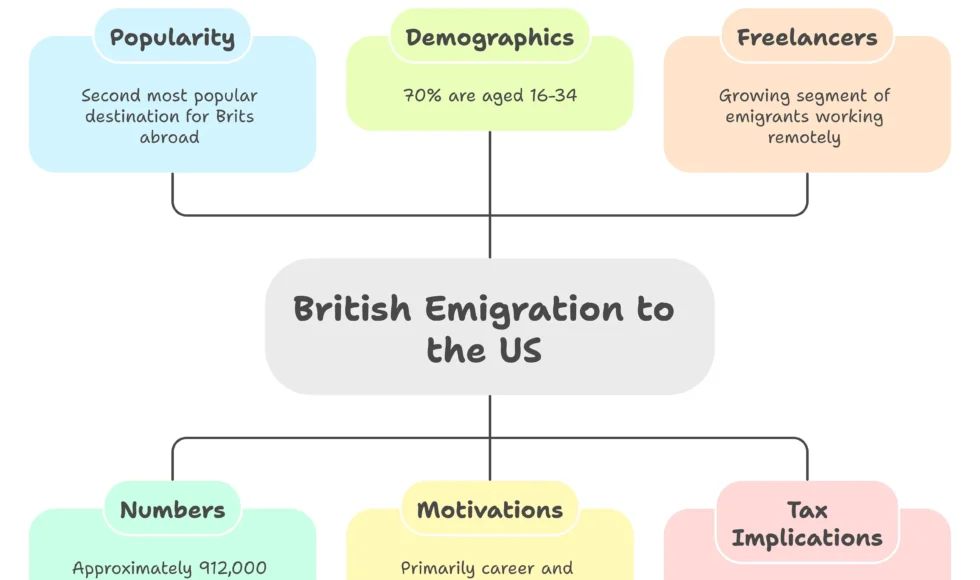

The United States is the top most popular destination for British citizens living abroad. According to United Nations population estimates from 2024, roughly 912,000 Brits call America home — behind only Australia. And the Oxford Migration Observatory’s data shows that around 70% of British emigrants are aged between 16 and 34, moving primarily for career and lifestyle reasons.

A growing slice of that group are freelancers. Designers, developers, writers, consultants — people whose work lives inside a laptop and whose clients don’t particularly care which time zone the laptop is in. The move feels clean. Same clients, same invoices, new postcode.

Except HMRC doesn’t see it that way. And neither does the IRS.

The Part That Catches People Out

There’s a widespread assumption that leaving the UK automatically ends your UK tax obligations. You’ve moved. You’re paying rent in Austin or Brooklyn. Your mornings smell like American coffee instead of PG Tips. Surely HMRC gets the message.

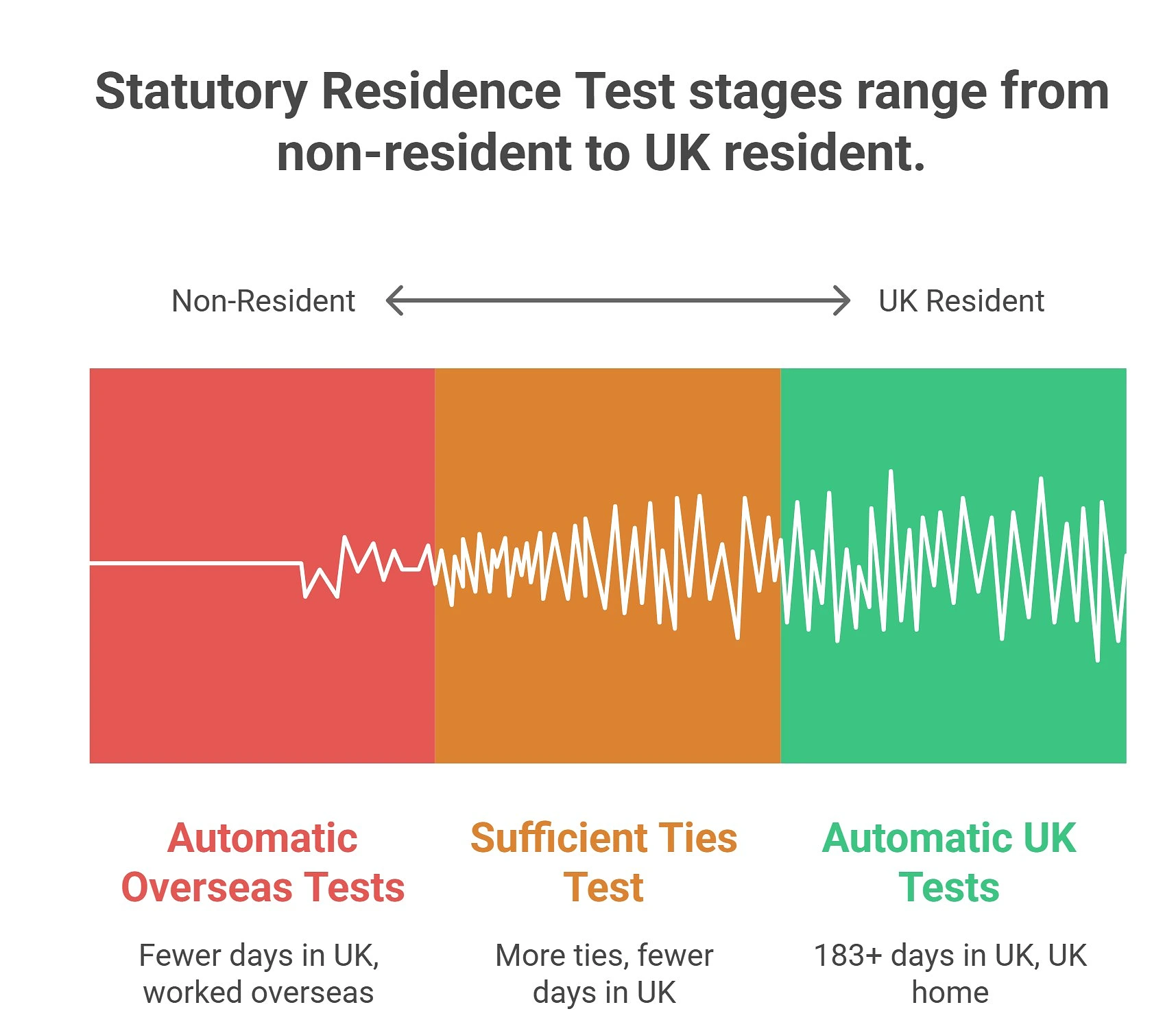

They don’t — not unless you’ve properly established non-residency through the Statutory Residence Test, which has been the legal framework for determining UK tax residency since April 2013.

How the Statutory Residence Test actually works

The SRT isn’t a single question. It’s a three-stage process, and HMRC runs through it in order:

Stage 1 — The automatic overseas tests. You’re automatically non-resident if you spent fewer than 16 days in the UK during the tax year (and were resident in at least one of the three preceding years), or fewer than 46 days (if you weren’t resident in any of the three preceding years), or you worked full-time overseas and spent fewer than 91 days in the UK with no more than 30 of those as working days.

Stage 2 — The automatic UK tests. You’re automatically UK resident if you spent 183 days or more in the UK, or your only home was in the UK for at least 91 consecutive days and you spent at least 30 days there.

Stage 3 — The sufficient ties test. If neither of the automatic tests gives a clear answer, HMRC counts your ties to the UK — family, accommodation, substantive work, 90-day presence in prior years, and country ties. The more ties you have, the fewer days you can spend in the UK before you’re pulled back into residency.

The critical thing most freelancers miss is that this isn’t optional or informal. You don’t tell HMRC you’ve left and they take your word for it. Your actual behaviour — days counted, ties maintained, homes kept — determines your status. And if you get it wrong, HMRC can tax your worldwide income as if you never left.

The Graphic Designer Who Moved to Portland

Picture this. You’re a freelance graphic designer. You’ve been working from Manchester for three years, billing UK and European clients through your sole trader registration. You move to Portland, Oregon in September 2025. You keep your UK bank account open. Your mum’s spare room still has your old desk in it. You fly back for Christmas and stay three weeks.

You assume you’re done with HMRC. You’re not.

Because you left mid-year, the tax year (6 April 2025 to 5 April 2026) is split. You may qualify for split-year treatment, which means you’re taxed as a UK resident only for the portion of the year before you left, and as non-resident for the rest. But split-year treatment isn’t automatic — it only applies in eight specific scenarios defined by HMRC, and you have to claim it on your Self Assessment return.

If you don’t qualify — say you came back too often or didn’t meet the full-time overseas work condition — you remain UK tax resident for the entire year. Every dollar you earned in Portland gets reported to HMRC as worldwide income. And you’re also reporting it to the IRS, because you’re now earning income on American soil.

That’s double taxation territory, and while the UK-US Double Taxation Agreement exists to prevent you paying full tax in both countries, navigating it requires knowing which country has primary taxing rights on which types of income — and claiming relief correctly on both returns.

The National Insurance Question Nobody Asks Until It’s Too Late

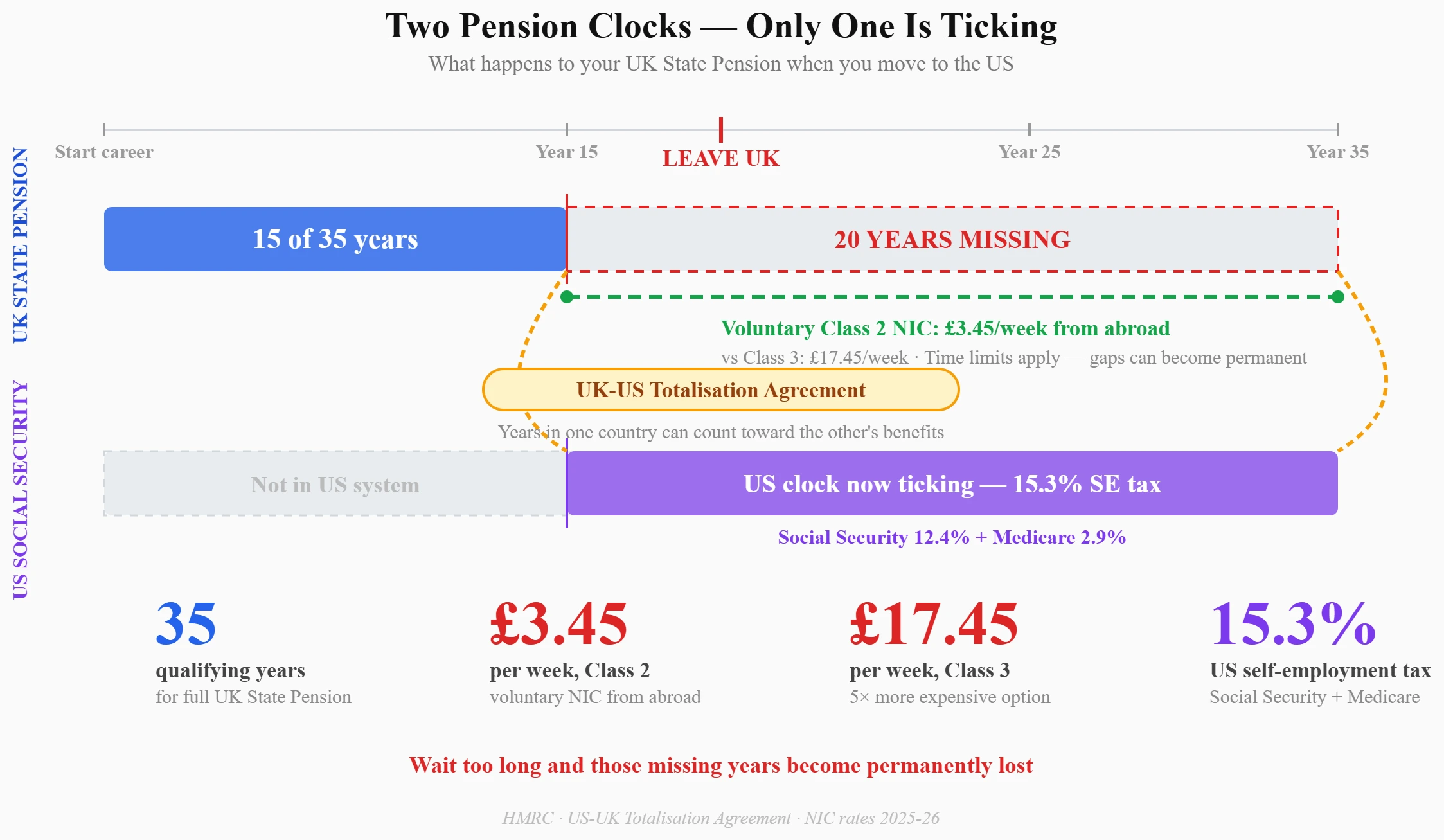

Income tax gets all the attention. National Insurance gets forgotten. And then twenty years later, you discover you’re six years short of the 35 qualifying years needed for a full UK State Pension.

When you leave the UK, your Class 2 and Class 4 NIC obligations stop — but your State Pension clock also stops ticking. You can make voluntary Class 2 or Class 3 contributions from abroad to fill the gaps, and Class 2 is significantly cheaper (roughly £3.45 per week compared to £17.45 for Class 3 in 2025-26).

The catch is that you typically need to have lived or worked in the UK immediately before going abroad, and there are time limits on how far back you can fill gaps. If you wait ten years to think about this, some of those years may be permanently lost.

Meanwhile, the US has its own social security system. If you’re self-employed in America, you pay self-employment tax at 15.3% on net earnings — covering Social Security (12.4%) and Medicare (2.9%). The UK and US do have a Totalisation Agreement that prevents you paying into both systems simultaneously and allows periods of coverage in one country to count towards benefits in the other. But you have to know it exists to use it.

What HMRC Actually Expects when you move abroad?

The departure process has specific steps that most freelancers either don’t know about or skip entirely.

Form P85 — you should complete this when you leave the UK. It tells HMRC your departure date and helps them calculate whether you’re due a refund for the year you left. It’s not legally mandatory for self-employed individuals in every case, but submitting it creates a clean record of your departure and avoids HMRC chasing you for returns they think you should still be filing.

Self Assessment — you’ll almost certainly need to file a return for the tax year in which you leave, and potentially for subsequent years if you still have UK-source income (rental property, UK clients paying into a UK account, dividends from a UK company). Being non-resident doesn’t automatically exempt you from Self Assessment. If you have UK-source income above £2,000, you’re still in the filing system.

Record keeping — HMRC can ask for evidence of your whereabouts. Keep records of your travel dates, your lease or utility bills in the US, and anything else that demonstrates where you were living and working. The SRT is tested on facts, and if HMRC queries your status three years later, you’ll need documentation to support your claim.

The IRS Side — Because America Taxes on Presence, Not Just Citizenship

This is where the two systems collide in a way that genuinely confuses people.

The UK taxes based on residency. If you’re non-resident, HMRC generally doesn’t tax your overseas freelance income — even if those clients are in London. The work isn’t being performed in the UK, so it falls outside HMRC’s reach.

The US taxes based on presence and residency (for non-citizens). If you meet the Substantial Presence Test — which counts days spent in the US over a three-year period — the IRS considers you a US tax resident and taxes your worldwide income. As a self-employed freelancer in the US, you’ll file a federal return, pay federal income tax on your earnings, pay self-employment tax (15.3%), and potentially owe state income tax depending on where you live. Texas and Florida have no state income tax. California charges up to 13.3%. Oregon goes up to 9.9%.

The UK-US Double Taxation Agreement determines which country has primary taxing rights. For self-employment income, the country where the work is performed generally has first claim. So if you’re freelancing from Portland for UK clients, the US taxes that income first, and the UK provides relief through the foreign tax credit or exemption — assuming you’ve properly established non-residency with HMRC.

Getting both sides right simultaneously is genuinely difficult without professional help. The two systems use different tax years (UK runs April to April; US runs January to December), different currencies, different definitions of deductible expenses, and different filing deadlines.

The Bits That Sound Small But Actually Matter

Your UK bank account. Keeping it open is fine and often practical, but receiving regular freelance income into a UK account while claiming to be non-resident can complicate your position. HMRC may view ongoing UK banking activity as a tie.

Your UK property. If you own a home in the UK and it remains available for your use, that counts as a tie under the SRT. Renting it out may actually help your non-residency case, because it’s no longer “available” for your personal use — but you’ll owe UK tax on the rental income as a non-resident landlord.

Visits back. Every day counts. Arriving at midnight and leaving the next day can still register as two days under certain counting rules. If you’re close to a threshold, a long Christmas visit could tip your residency status for the entire tax year.

Healthcare. You lose NHS entitlement once you’re no longer ordinarily resident. The US has no equivalent public system — you’ll need private health insurance, and if you’re self-employed, that’s another cost that doesn’t appear on the freelance income comparison spreadsheet.

The Honest Summary

Moving to America as a British freelancer is entirely doable. Hundreds of thousands of Brits have done it. The work translates, the clients don’t care, and the lifestyle change can be worth every complication.

But the tax position is not simple, and it’s not something you can sort out retrospectively without cost. The Statutory Residence Test, the split-year rules, National Insurance gaps, the US self-employment tax, state-level obligations, and the Double Taxation Agreement all interact in ways that require planning before departure — not troubleshooting after.

As the old proverb goes — look before you leap. And in this case, look at both countries’ tax codes before you book the flight.

This article is for informational purposes only and does not constitute tax or legal advice. Tax rules differ by jurisdiction and individual circumstances. Readers should consult a qualified tax professional before making decisions about working abroad or changing their tax residency.