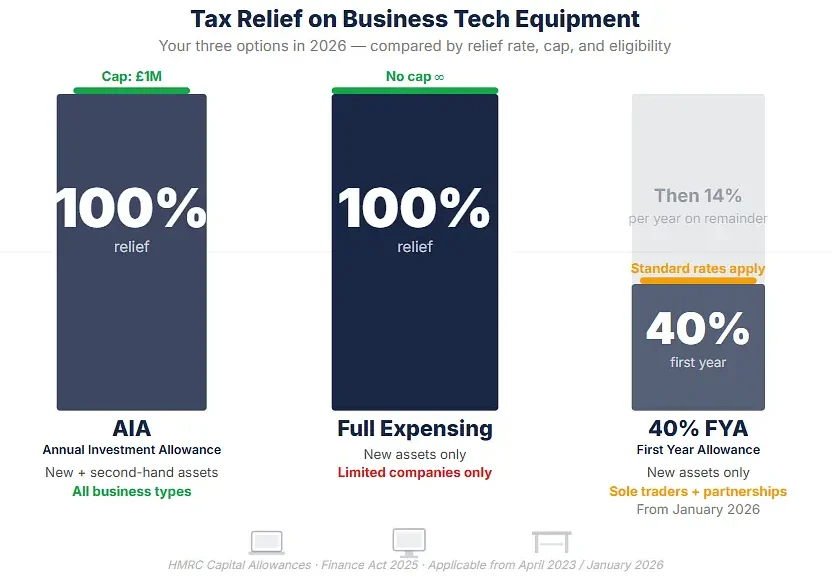

If your business buys a laptop, a portable monitor, a desk, a printer or pretty much any piece of equipment that gets used for work, you can claim tax relief on it. The main route is the Annual Investment Allowance which gives you 100% relief on qualifying purchases up to one million pounds per year. That means if your limited company spends five thousand pounds on tech equipment, the full five thousand comes off your taxable profits and at 25% corporation tax that’s twelve hundred and fifty pounds back in your pocket immediately.

Most small businesses never come close to the one million cap which means in practice every tech purchase you make for the business gets fully deducted in the year you buy it. No spreading the cost over multiple years, no complicated depreciation calculations, just straight off the top of your taxable profit.

That’s the simple version. The detail underneath it matters though, because the type of business you run, whether you’re incorporated or not and when you bought the equipment all change which relief applies and how much you actually save.

Annual Investment Allowance — The One Most Businesses Should Use First

The AIA has been permanently set at one million pounds since the Spring Budget 2023. It covers what HMRC classifies as “plant and machinery” which sounds industrial but actually includes almost everything a modern business buys to operate:

- Computers and laptops

- Monitors, portable screens and display equipment

- Desks, chairs and office furniture

- Printers, scanners and copiers

- Phones and headsets

- Servers, networking equipment and routers

- Software (where it’s treated as capital expenditure rather than a subscription)

The relief is available to limited companies, sole traders and partnerships. You claim it in the accounting period where the equipment first becomes available for use, not when you order it, not when you pay for it but when it’s actually ready to be used in the business. That timing distinction catches people out sometimes, ordering a batch of laptops in March but not receiving them until April means the relief falls into the following year.

Worked example

A design agency buys three new workstations at eight hundred pounds each, two portable monitors at two hundred and fifty each, ergonomic chairs at four hundred each for three staff and a network-attached storage unit for fifteen hundred. Total spend comes to roughly five thousand six hundred pounds.

Under AIA all of that is deducted from taxable profits in year one. At the 25% corporation tax rate that’s fourteen hundred pounds saved. At the 19% small profits rate (profits under fifty thousand) it’s just over a thousand. Either way the full cost comes off your profits immediately.

Full Expensing — For Limited Companies Buying New Equipment

Full expensing became permanent from April 2023 and it gives limited companies 100% first-year relief on new main-rate plant and machinery with no upper cap. That “no cap” part is what distinguishes it from the AIA which tops out at one million.

For most small businesses the practical difference between AIA and full expensing is minimal because you’re unlikely to spend over one million on equipment in a single year. But there are two important distinctions worth knowing:

Full expensing only applies to new assets. If you buy a second-hand server rack or refurbished laptops, full expensing doesn’t cover them. AIA does, it works on both new and second-hand equipment without any restriction.

Full expensing is companies only. Sole traders and partnerships cannot claim it. They use AIA instead and if they exceed the one million AIA limit they now have access to the new 40% first-year allowance introduced in January 2026 which didn’t exist before.

Full expensing has clawback rules on disposal. If you sell equipment that you claimed full expensing on, the disposal value is immediately taxable. AIA doesn’t have this specific clawback mechanism in the same way.

For a small limited company buying new tech equipment under one million pounds, AIA and full expensing produce the same tax result. Use whichever your accountant prefers to work with. The difference only really matters at scale or when second-hand assets are involved.

The New 40% First-Year Allowance from January 2026

This one came out of the Autumn Budget 2025 and it’s specifically aimed at businesses that couldn’t benefit from full expensing, mainly sole traders, partnerships and businesses leasing assets.

From 1 January 2026 qualifying expenditure on new main-rate plant and machinery attracts a 40% first-year allowance. The remaining 60% goes into the writing-down allowance pool at the new reduced rate of 14% (down from 18%, also effective from April 2026).

In real terms this means a sole trader who buys three thousand pounds worth of new office equipment and has already used their AIA allocation elsewhere can deduct twelve hundred in year one through the 40% FYA and then claim writing-down allowances on the remaining eighteen hundred at 14% per year after that.

It’s not as generous as AIA or full expensing but for unincorporated businesses with heavy capital expenditure it’s a meaningful improvement over the old position where everything beyond the AIA limit went straight into the writing-down pool at 18% with no accelerated first-year relief at all.

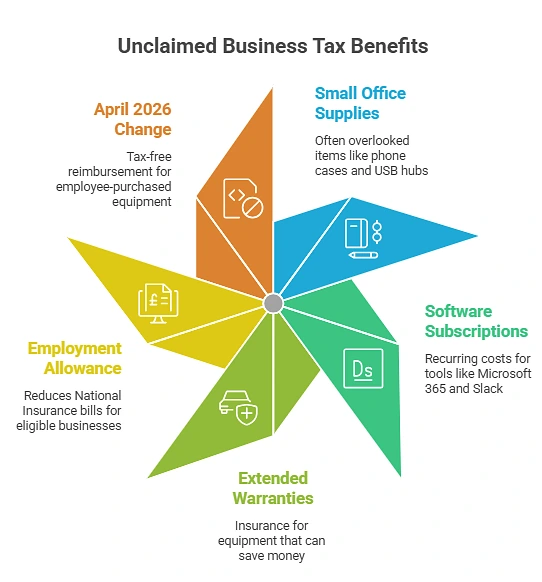

The April 2026 Reimbursement Rule Change — This One Is New

Buried in the Autumn Budget 2025 detail is a change that directly affects remote and hybrid workers and the businesses that employ them.

Currently if an employer provides equipment like a monitor or headset for an employee working from home, that’s tax-exempt. But if the employee buys the same monitor themselves and the employer reimburses them, HMRC treats that reimbursement as a taxable benefit in kind. The employee pays tax on it and the employer pays Class 1A National Insurance on it. Same monitor, same business purpose, different tax treatment just because of who handed over the card at checkout.

From April 2026 that distinction disappears. The legislation is being extended so that reimbursements for employee-purchased equipment used for work are treated the same as employer-provided equipment. Tax-free for the employee, no NIC liability for the employer.

This is a genuine practical change for any business with remote or hybrid staff. If your employees have been buying their own portable monitor, keyboards, headsets or desk setups and expensing them back, the tax treatment just got significantly simpler and cheaper for both sides.

What Sole Traders and Freelancers Claim Differently

If you’re a sole trader using cash basis accounting, the rules change. Under cash basis you don’t claim capital allowances at all on most equipment because you simply deduct the purchase as a business expense in the year you pay for it. The only exception is cars which still go through the capital allowances system regardless of your accounting method.

That means a freelance developer who buys a laptop for nine hundred pounds under cash basis just puts it through as a business expense. No AIA claim, no depreciation pool, no writing-down allowances. Just a straight deduction. For most small sole traders this is simpler and produces the same economic result.

If you’re on accruals basis as a sole trader then capital allowances apply in the same way as for a limited company, AIA up to one million, the new 40% FYA from January 2026 for anything beyond that and writing-down allowances at the reduced 14% rate from April 2026.

There’s also the flat-rate working from home deduction. If you work from home you can claim a flat rate of six pounds per week (three hundred and twelve per year) without keeping receipts. Or you can calculate your actual home office costs, heating, lighting, broadband apportioned by business use, and claim the real figure if it’s higher. The flat rate is simpler but for anyone running significant equipment from a home office the actual calculation usually produces a bigger deduction.

The Bits That People Forget to Claim

Small items add up over a year and most of them qualify. Phone cases, USB hubs, cables, mouse mats, screen cleaning kits, external hard drives, SD cards. Individually they’re five or ten pounds but across a year for a small team they might total three hundred to five hundred pounds of unclaimed deductions.

Software subscriptions like Microsoft 365, Adobe Creative Cloud, Slack, Zoom and accounting packages are revenue expenses not capital expenditure so they don’t go through the capital allowances system at all. They’re simply deducted as business expenses against your profits in the year you pay them. The same applies to cloud hosting, domain renewals and SaaS tools.

Extended warranties and insurance on business equipment are also deductible as revenue expenses. If you bought a premium care plan when you picked up that new workstation, that cost comes off your profits in the year you paid it.

The Employment Allowance is worth mentioning here too even though it’s not directly about equipment. If your business employs staff and your employer NIC bill is under one hundred thousand pounds you can claim up to five thousand pounds off your annual employer National Insurance bill. That’s five thousand pounds freed up that could go toward the tech budget.

This article is for informational purposes only and does not constitute tax or accounting advice. Tax rules and allowances are subject to change. Readers should consult a qualified accountant or tax adviser for guidance specific to their business circumstances.