Key Points

- The Vaping Products Duty (VPD) takes effect on 1 October 2026, marking the first time e-liquids have carried excise duty in the UK.

- The flat rate is £2.20 per 10ml of vaping liquid, charged on volume regardless of nicotine strength — including nicotine-free products.

- A Vaping Duty Stamps scheme launches alongside VPD, requiring physical stamps with digital tracking on all retail packaging.

- Criminal offences apply for selling, importing, or possessing unstamped vaping products, with potential custodial sentences.

- HMRC registration for manufacturers and importers opens 1 April 2026, with a recommended 45 working days for approval.

- Tobacco duties will rise by a commensurate amount to preserve the financial incentive for smokers to switch to vaping.

- The OBR projects the duty will affect an estimated 5.1 million individuals who currently vape in the UK.

Where there’s smoke, there’s tax. Or in this case, where there’s vapour. The UK government has legislated what the vaping industry spent years expecting — a dedicated excise duty on e-liquids, structured to sit alongside existing alcohol and tobacco excise frameworks. The provisions are contained in Finance Bill 2025-26, announced at Autumn Budget 2025, and they arrive barely sixteen months after the single-use disposable vapes ban took effect on 1 June 2025.

The two measures together represent the most significant regulatory overhaul the UK vaping market has faced since the Tobacco and Related Products Regulations transposed the EU’s Tobacco Products Directive into domestic law back in 2016.

How the Duty Is Structured

In the 2024 consultation, the government first proposed a three-tier rate framework related to nicotine strength. That was scrapped. The Treasury rejected that proposal in favour of a flat tax rate of £2.20 per 10 millilitres (ml) of vaping liquid — or 22p per ml — which would have applied the same charge regardless of the nicotine content.

Nicotine salt liquid attracts £2.20 in duty on a 10ml bottle. The 100ml shortfill bottle sells for £22.00 A 2ml prefilled pod costs nowt if you check the price under “Other” and select the “72mg nicotine, diluted at your ratio of choice” option; a bottle of zero-nicotine e-liquid pays out the same per-millilitre as one containing 20mg. Volume, not composition, determines the charge.

VAT then comes on top of the duty-inclusive price. An industry forecast has predicted that standard 10ml bottles will cost between £5.50 and £7.00 after October 2026, which is around double the current prices on shelves. Shortfills are hit hardest proportionally, with duty alone on a 100ml bottle costing over £20 before VAT is applied.

According to the Treasury, the flat-rate approach is in line with international practice and would reduce compliance by businesses and enforcement by HMRC. The tiered alternative would have imposed nicotine testing at various points in the supply chain — cost and complexity burdens that consultation responses flagged as impractical.

The Vaping Duty Stamps Scheme

Running parallel to the duty itself, HMRC is introducing a Vaping Duty Stamps (VDS) scheme modelled on existing tobacco stamp requirements. Every vaping product manufactured in or imported into the UK must carry a physical duty stamp on its retail packaging from 1 October 2026.

The stamps are produced by Cartor Security Printers, HMRC’s appointed supplier. They come in wet (pre-glued) and dry formats, with a minimum order of 1,000 stamps per reel. Each stamp must seal the packaging so the product cannot be opened without damaging either the packaging or the stamp. Stamps cannot be reused.

Between 1 October 2026 and 31 March 2027, transitional stamps — carrying physical security features but without the digital element — are accepted. From 1 April 2027, all vaping products outside duty suspension must carry stamps with a digital tracking feature, such as a QR code. Businesses at each point in the supply chain are responsible for scanning the stamp, allowing HMRC to track product movement from manufacture or import through to retail sale.

Overseas manufacturers must appoint a UK representative to apply for stamp approval and purchase stamps on their behalf. HMRC can refuse or revoke stamp purchasing rights, and the scheme includes provisions for limiting stamp volumes based on sales forecasts to prevent forestalling — the practice of stockpiling goods ahead of a duty increase.

Offences and Enforcement Powers

The legislation introduces both civil penalties and criminal offences for non-compliance. These include:

- Failure to register with HMRC before manufacturing or importing vaping products.

- Failure to file returns or pay duty within prescribed periods.

- Possession, sale, importation, or transport of unstamped vaping products.

- Evasion or fraudulent activity under the existing excise fraud provisions in the Customs and Excise Management Act 1979.

Criminal offences carry possible custodial sentences. Courts can also issue orders banning premises from operating as vape shops where criminal dealing in stamps is proven — a provision aimed at preventing organised crime groups from cycling through different personnel or company names at the same location.

HMRC gains new information-sharing powers to exchange data with other public authorities responsible for vaping product enforcement. Unstamped goods are liable to seizure, and HMRC can remove legitimate stock from premises found to hold unstamped products alongside stamped inventory.

The long arm of the law, in this case, extends right down to the individual retail shelf.

Revenue Projections and Policy Rationale

OBR-certified revenue forecasts are published in Budget 2025. Initial exchequer costs of £50 million in 2025-26 are expected, owing to implementation and transitional effects, before providing net revenue in the following years. HMRC has estimated total delivery costs could reach around £140 million, including: * ‘Around’ £20 million (c $26mn) on IT systems; * c£120m for resourcing and staffing during 2025-26 to 2029-30 period of implementation; up to c.£10m for Border Force enforcement

The policy rationale straddles two places. Law 1: Public health: The government wants to make vaping and heat-not-burn products less affordable and desirable for young people and non-smokers, while still maintaining incentives for adult smokers switching. The Chief Medical Officer’s position still is that those who do not smoke or vape should not start.

Second, on the revenue side: tobacco duty is expected to bring in around £8.1bn in 2025-26. To keep the price discrepancy between smoking and vaping, tobacco duties will increase proportionally with VPD when it is introduced. There is a risk, without that parallel increase, that the result will be cheaper cigarettes relative to newly taxed vape products, but this could push some vapers back to combustible tobacco — the public health outcome the Treasury itself poor and flagged in their impact assessment.

HMRC’s own analysis (p13) redresses this tension directly: heavy vapers will bear the greatest burden and one possible behavioural outcome — to avoid it — is migration back to tobacco products. The circular tobacco duty increase is intended to close that risk off.

What Changed Before the Duty — The Disposable Vapes Ban

The VPD doesn’t arrive in isolation. Single-use disposable vapes became illegal to sell or supply in the UK from 1 June 2025, including nicotine-free disposables. That ban eliminated the cheapest entry point to vaping — typically £4–£6 per device — and pushed millions of consumers toward prefilled pod systems and refillable kits paired with bottled e-liquids.

The duty now lands on top of that transition. Consumers who moved from disposables to refillable systems between June 2025 and October 2026 will see the cost of their chosen format increase again, though refillable kits paired with 10ml bottles remain the most cost-efficient format on a per-millilitre basis, even after duty is applied.

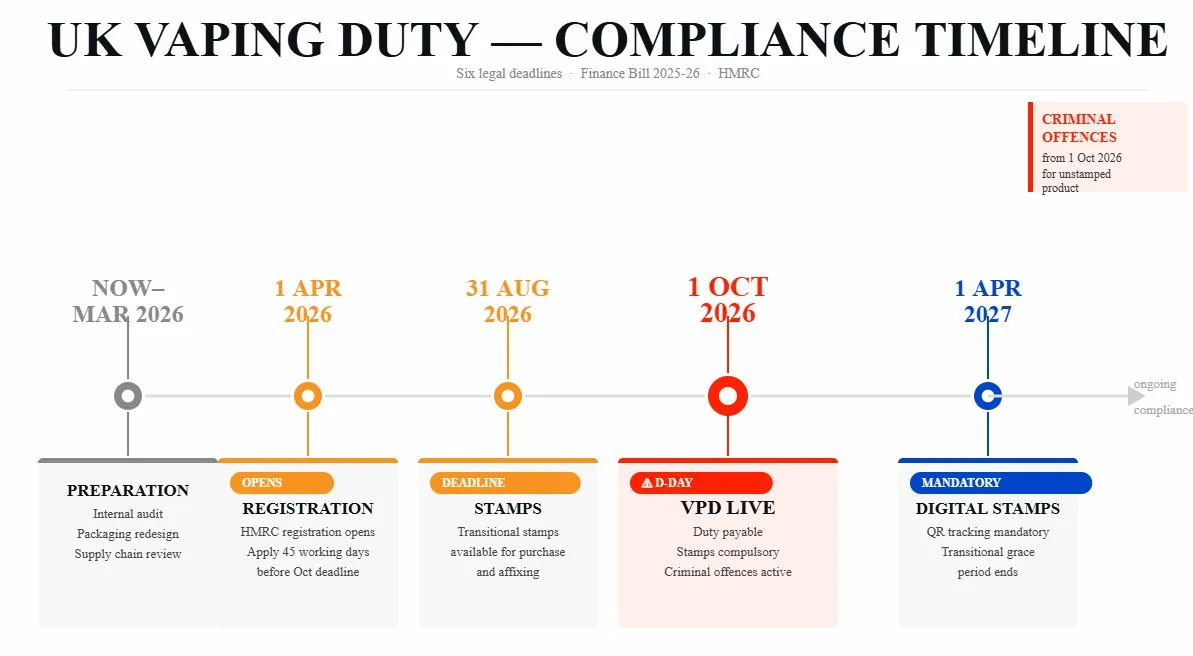

The Registration and Compliance Timeline

The practical timeline for affected businesses runs as follows:

- Now through March 2026: Familiarisation, internal audit, packaging redesign for stamp compatibility, supply chain review.

- 1 April 2026: HMRC registration opens for VPD and VDS approval. Applications recommended at least 45 working days before the duty start date.

- Until 31 August 2026: Transitional stamps available for purchase and affixing.

- 1 October 2026: VPD takes effect. Duty payable on all products released for consumption. Stamps compulsory on retail packaging. Criminal offences and civil penalties enforceable.

- 1 April 2027: Full digital stamps mandatory on all vaping products outside duty suspension. Grace period for unstamped transitional stock ends.

Secondary legislation setting out further operational details is anticipated in March 2026. Monthly duty returns will be required from registered businesses, and HMRC has indicated that compliance monitoring will be active from the outset, with a “test and learn” enforcement exercise in the early months.

The Broader Excise Context

The VPD fits nicely into a familiar UK fiscal template. In the 2023 Budget, it announced alcohol duty reforms which restructured duties on products according to their alcohol content rather than by category. Duty on tobacco has been raised above inflation every year for a decade. All three share a similar principle: volume-based or content-based excise duties levied at production or import point, collected through current HMRC infrastructure mechanisms and enforced via a combination of civil penalties, criminal sanctioning and physical marking schemes.

For vaping, the regulatory edifice is now built. These include the Tobacco and Related Products Regulations that address product standards, ingredient limits and packaging requirements. The single-use ban addresses format. The VPD addresses taxation. And the VDS tackles enforcement and traceability.

The mills of the gods grind slowly, but they grind exceedingly fine. After a decade of relatively light-touch regulation, compared with tobacco, the vaping industry now sits under a framework that bears in most material respects the stamp of its combustible predecessor.

This article is for informational purposes only and does not constitute legal, tax, or regulatory advice. Legislation and HMRC guidance are subject to change. Businesses and individuals should consult qualified professionals for advice specific to their circumstances.