Key Takeaways — The Quick Verdict

Before we get into the full breakdown, here’s what the numbers actually show when you compare a UK Ltd against a US LLC at three profit levels:

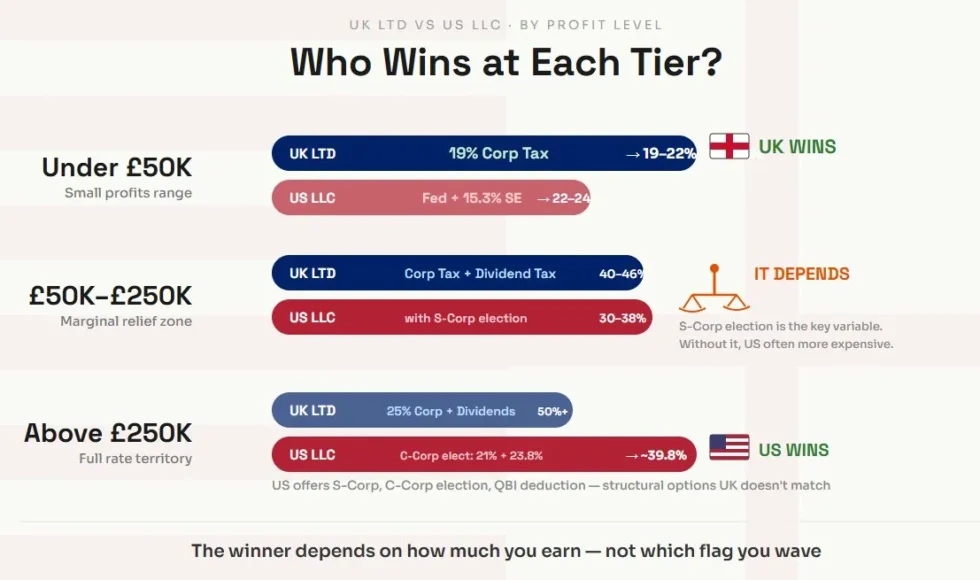

- Profit under £50,000 → UK Ltd wins. Corporation Tax sits at 19%. A US LLC owner pays federal income tax plus 15.3% self-employment tax, pushing the effective rate to 22–24% before state taxes. The UK leaves more in the founder’s pocket at this level.

- Profit between £50,000 and £250,000 → It depends on the US structure. If the US LLC elects S-Corp taxation, the combined burden can come in lower than the UK’s Corporation Tax plus dividend extraction tax (which climbs into the low-to-mid 40s). Without that election, the US is often more expensive.

- Profit above £250,000 → The US offers more flexibility. The flat 21% C-Corp rate, S-Corp election, and QBI deduction give US founders structural options the UK doesn’t match. UK Corporation Tax locks at 25%, and dividend extraction can push the combined burden past 50%.

- Hidden difference that changes everything: A UK Ltd pays tax as a company, then the owner pays again on extraction. A US LLC passes profit straight to the owner’s personal return — one layer, but self-employment tax hits hard unless you elect otherwise.

Now, the full picture.

They say the only certainties in life are death and taxes. But nobody mentions that the amount of tax depends enormously on which side of the Atlantic you registered your business.

Most trusted attorneys in Charleston SC think that it is less about lower tax in other countries and more about where the breakpoints sit at different revenue levels. A UK director wondering about a US LLC. An American entrepreneur eyeing a UK Ltd. Both assuming the grass is greener.

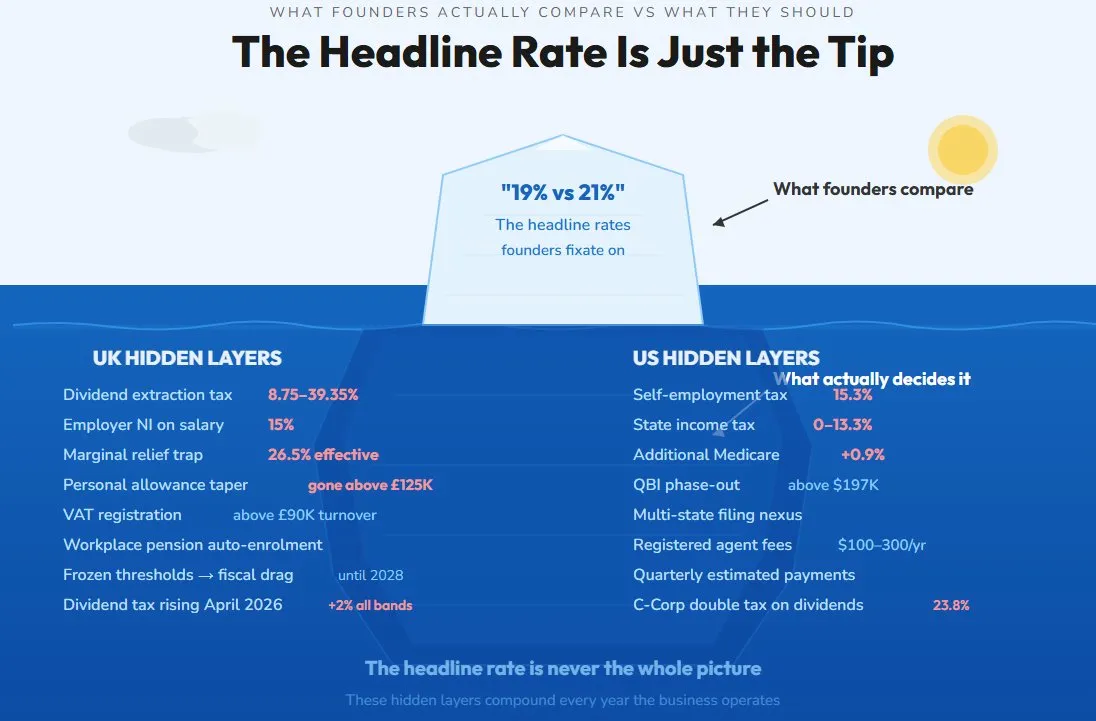

The truth, as Henderson put it during our discussion, is less about which country has lower tax and more about where the breakpoints sit at different revenue levels. “Most founders fixate on the headline rate,” he said. “They hear 19% in the UK or 21% in the US and think that’s the whole picture. It never is.”

He’s right. And once you lay the actual numbers side by side — not the headlines, the real effective burden at specific profit levels — the comparison gets uncomfortable for both sides.

The Structural Difference That Changes Everything

Before the numbers make sense, the mechanics need explaining. And this is where most comparisons fall apart, because a UK Ltd and a US LLC don’t work the same way at all.

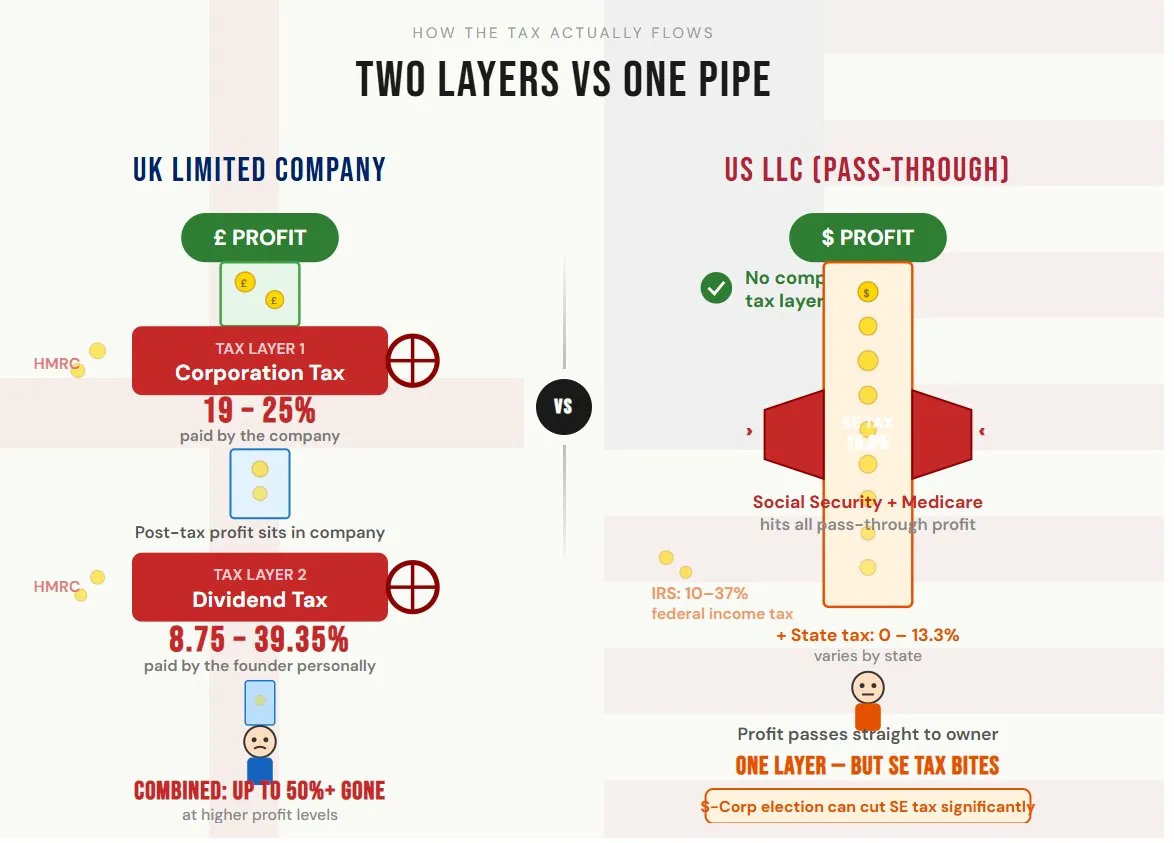

A UK limited company is a separate taxable entity. It earns profit, pays Corporation Tax on that profit, and then the director or shareholder extracts what’s left through salary, dividends, or a combination. The company pays its tax. The individual pays theirs. Two separate events.

A US LLC, by default, is a pass-through entity. The business itself pays no federal income tax. Instead, the profit lands directly on the owner’s personal tax return — Schedule C for a single-member LLC, or K-1 allocations for multi-member setups. The owner then pays individual income tax on that profit, plus self-employment tax covering Social Security and Medicare.

Henderson flagged this as the single biggest misconception he sees. “People compare a 19% UK rate to a 21% US corporate rate and think the LLC is more expensive. But the LLC isn’t paying corporate tax at all — unless it elects to. The owner is paying personal rates on business profit, and those rates start at 10% and go up to 37%.”

That pass-through mechanism is both the LLC’s greatest advantage and its sharpest edge.

Under £50,000 in Profit — Where the UK Has a Clear Run

At the smaller end, the UK Ltd has a straightforward deal. Profits up to £50,000 attract the small profits rate of 19% Corporation Tax. No marginal relief calculations, no complexity. A company earning £40,000 in taxable profit pays £7,600 in Corporation Tax.

The extraction question adds another layer. If the director takes a salary up to the personal allowance (£12,570) and draws the rest as dividends, the combined personal tax on extraction is relatively modest — the dividend allowance and basic rate dividend tax at 8.75% (rising to 10.75% from April 2026 following the Autumn Budget) keep the overall burden manageable.

For a US single-member LLC earning the equivalent of £40,000 (roughly $50,000), the picture is different. Federal income tax at the 22% bracket applies to most of that profit after the standard deduction. But then self-employment tax — 15.3% on 92.35% of net earnings — stacks on top. That’s the part most people don’t see coming.

On $50,000 of LLC profit, a single filer in the US would owe roughly:

- ~$4,000–$5,000 in federal income tax (after standard deduction and the 20% QBI deduction)

- ~$7,065 in self-employment tax

Total federal burden somewhere around $11,000–$12,000 on $50,000 of profit. That’s an effective rate pushing 22–24% before state taxes even enter the equation. States like South Carolina add their own income tax on top.

The UK Ltd owner at £40,000 profit, extracting through salary and dividends efficiently, typically faces a combined company-plus-personal burden closer to 19–22%.

At this level, the UK generally leaves more in the founder’s pocket. The Corporation Tax rate is lower than the combined US federal-plus-SE burden, and the salary/dividend extraction mechanism in the UK creates efficiency that pass-through taxation doesn’t offer.

Henderson agreed but added a caveat worth noting. “The QBI deduction — the 20% qualified business income deduction — was recently made permanent under the One Big Beautiful Bill Act. That helps US LLC owners more than people realise at this level. Without it, the gap would be wider.”

£50,000 to £250,000 — The Marginal Relief Zone vs the Bracket Creep

This is where both systems start getting complicated, and where founders on both sides start making planning mistakes.

In the UK, profits between £50,001 and £250,000 fall into the marginal relief band. Corporation Tax is technically charged at 25%, but marginal relief reduces the effective rate on a sliding scale between 19% and 25%. At £150,000 profit, the effective Corporation Tax rate works out to roughly 24%. The marginal rate on profits within this band can actually spike to 26.5% — higher than the main rate — which catches a lot of business owners off guard.

Then there’s the extraction cost. Dividends above the basic rate band get taxed at the higher rate — currently 33.75%, rising to 35.75% from April 2026. A director pulling £100,000 in dividends after Corporation Tax starts seeing a combined effective rate that climbs into the low-to-mid 40s when you account for both layers.

The US LLC at equivalent profit levels faces a different kind of squeeze. On $200,000 of pass-through income (roughly £160,000), the federal picture looks something like:

- Federal income tax in the 32% bracket on upper portions of income

- Self-employment tax of 15.3% on the first $160,200 (the 2025 Social Security wage base), then 2.9% Medicare above that

- The QBI deduction helps — it knocks 20% off qualified business income before calculating federal tax — but it starts phasing out for service businesses above $197,300 (single filer)

- State income tax varies wildly. South Carolina charges up to 6.4%. Some states charge nothing.

Henderson raised something practical here. “At this level, most US attorneys advise the LLC to elect S-Corp taxation. You pay yourself a reasonable salary — say $80,000 — and the remaining profit comes through as distributions that aren’t subject to self-employment tax. That alone can save $6,000 to $12,000 a year compared to a default LLC.”

That’s a genuine structural advantage. The UK doesn’t have an equivalent manoeuvre. You can’t split your income between Corporation Tax and self-employment exemption in the same way. The salary-plus-dividend extraction method is the UK’s version, but it doesn’t avoid National Insurance with the same surgical precision.

At this tier, the comparison tightens. The UK’s combined Corporation Tax plus dividend extraction burden runs roughly 40–46% on profit taken out by a higher-rate taxpayer. The US LLC (with S-Corp election) can achieve effective rates in the 30–38% range depending on the state. Without the S-Corp election, the US burden at this level can exceed 45% once self-employment tax and state tax combine.

Above £250,000 — Where the Maths Diverge Sharply

At the top end, the UK structure becomes brutally simple. Corporation Tax locks in at 25% on all profit. No marginal relief. No sliding scale. Just 25%.

But getting the money out is where it stings. Dividends above the higher rate band face the additional rate — 39.35% from April 2026 (up from the current 39.35%, itself increased from 38.1% pre-Budget). A director extracting £300,000 of post-Corporation Tax profit as dividends faces a combined effective rate that can touch 50% or above depending on the interaction between Corporation Tax, income tax bands, and the personal allowance taper (which removes the £12,570 allowance entirely once income exceeds £125,140).

The November 2025 Autumn Budget made this worse in a quieter way. Dividend tax rates went up by 2 percentage points across all bands from April 2026. Savings income tax went up by 2 percentage points from April 2027. And income tax thresholds remain frozen until 2028, meaning more profit gets dragged into higher bands through fiscal drag alone.

For the US LLC above $250,000, the picture depends heavily on the chosen structure:

Default LLC (pass-through): Federal income tax hits the 35% bracket above roughly $243,725 (single filer), and 37% above $609,350. Self-employment tax adds 2.9% Medicare on all earnings above the Social Security cap ($160,200 in 2025, $184,500 in 2026), plus a 0.9% Additional Medicare Tax above $200,000. State taxes add 0–13.3% depending on location. Combined effective rate can exceed 50% in high-tax states like California or New York.

S-Corp election: Significantly reduces the self-employment tax bite. But the IRS requires “reasonable compensation,” and at this profit level, the salary portion can’t be trivially small. Still, the savings on distributions are substantial.

C-Corp election: The LLC can elect to be taxed as a C-Corporation at a flat 21% federal rate. That’s attractive on paper, but dividends paid to owners get taxed again at the shareholder level — 20% for qualified dividends plus the 3.8% Net Investment Income Tax. Total combined burden on extracted profit: roughly 39.8% (21% corporate + 23.8% on what’s left). Still lower than the UK’s combined burden in many scenarios.

Henderson made an interesting observation here. “Above $500,000 in profit, we’re increasingly seeing LLC owners elect C-Corp treatment specifically to access the flat 21% rate. They reinvest rather than distribute, and the retained earnings compound at a lower tax cost than any pass-through structure would allow.”

That option doesn’t exist in the UK. Corporation Tax is 25%, full stop. There’s no election to access a lower rate. And the retained earnings still eventually face extraction tax when they come out.

At this level, the US generally offers more structural flexibility — particularly through entity election — to manage the overall tax burden. The UK’s simplicity comes at the cost of a higher combined rate for business owners who need to extract profit.

The Hidden Costs That Don’t Appear in Rate Comparisons

Tax rates are only part of the equation. Both systems carry costs that founders rarely factor in at the formation stage.

UK compliance costs: Companies House filing (£13 annual Confirmation Statement), Corporation Tax return preparation, personal self-assessment for the director, potential VAT registration above £90,000 turnover, workplace pension auto-enrolment obligations, payroll reporting for director salary. The regulatory burden is centralised — one Companies House, one HMRC — but the layers add up.

US compliance costs: State annual reports (varies by state — South Carolina charges $0 for the annual report but requires a $25 filing), registered agent fees, federal tax returns, state tax returns, quarterly estimated tax payments, potential nexus issues if operating in multiple states. There’s no single federal registry. Each state has its own rules, its own fees, and its own deadlines.

Henderson noted this as a frequent source of frustration for his clients. “The state-by-state complexity in the US is something UK business owners genuinely struggle to believe. You can owe filing obligations in states where you don’t have an office, purely because you have customers there.”

Then there’s the formation cost itself. A UK Ltd can be registered through Companies House for £12 online. A US LLC formation fee ranges from $50 (Kentucky) to over $500 (Massachusetts), plus ongoing registered agent costs that typically run $100–$300 per year.

What the Revenue Tiers Actually Tell Us

The comparison isn’t about one system being universally better. It’s about where each structure creates or destroys value relative to the founder’s actual situation.

Below £50,000 profit: The UK Ltd’s 19% Corporation Tax plus efficient salary/dividend extraction generally beats the US LLC’s combined federal income tax plus 15.3% self-employment tax. The UK structure is simpler and cheaper to maintain at this level.

£50,000 to £250,000 profit: The comparison narrows. The US LLC with an S-Corp election can achieve lower combined effective rates than the UK Ltd once extraction tax is included. Without the S-Corp election, the US is often more expensive due to uncapped self-employment tax.

Above £250,000 profit: The US offers more structural options — S-Corp election, C-Corp election, QBI deduction strategies — that can produce lower combined rates than the UK’s fixed 25% Corporation Tax plus increasingly heavy dividend taxation. The UK’s simplicity becomes a constraint rather than a benefit.

None of this accounts for personal circumstances, residency status, treaty relief, state-specific variations, or the dozens of other variables that change the outcome for any individual founder. The devil, as they say, is in the detail — and when it comes to cross-border tax planning, the detail has its own details.

The point isn’t to pick a winner. It’s to understand that the choice between an LLC and a Ltd isn’t a branding decision or a paperwork preference. It’s a tax architecture decision that compounds over every year the business operates.

Getting it right at formation is considerably cheaper than restructuring after the fact.

This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Tax rules vary by jurisdiction and individual circumstances. Readers should consult a qualified professional before making decisions about business formation or tax structuring.