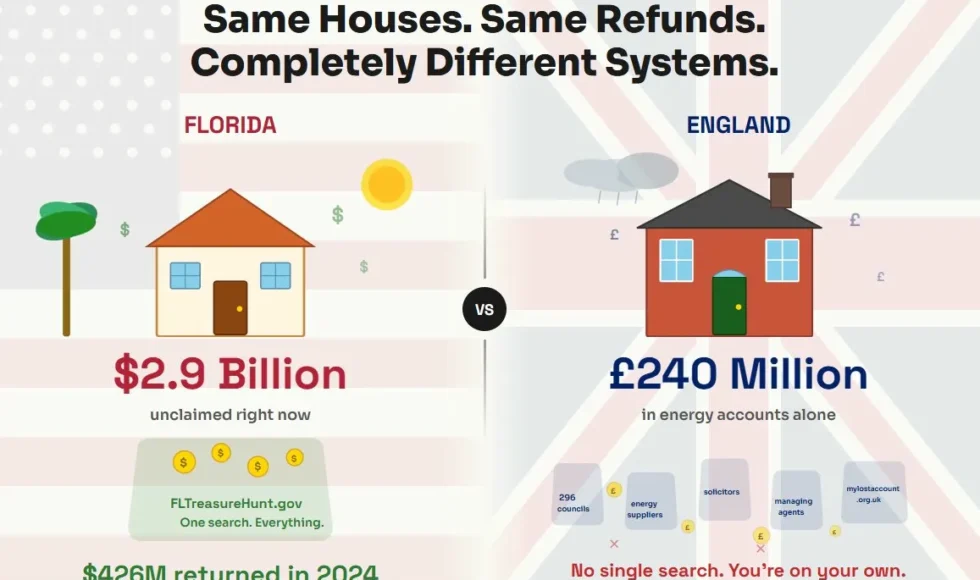

Florida is sitting on $2.9 billion in unclaimed property right now. Across England, Scotland and Wales, £141 million in council tax overpayments belongs to over 808,000 households who haven’t collected it. And tucked away inside 1.9 million closed UK energy accounts? Another £240 million nobody’s come back for.

Two countries. Completely different property systems. Same result — homeownership creates dozens of financial touchpoints, and at every single one, money can slip away without anyone noticing.

Escrow surpluses after a refinance. Council tax credits sitting with a council you moved away from six years ago. A buildings insurance refund that got swallowed by your mortgage company. An HOA deposit in Tampa or a leasehold service charge surplus in Manchester — the mechanisms are different, but the outcome is identical. Somebody owes you money, and nobody’s told you.

This is a side-by-side breakdown of how each country handles lost homeowner refunds, where the systems work, where they fail, and which side actually does it better.

Property Tax Overpayments vs Council Tax Credits: Which System Returns Your Money Faster?

Florida runs property taxes through county tax collectors. Overpayments happen for predictable reasons — value reassessments, delayed exemptions, duplicate payments during a refinance. When a refund goes unclaimed (usually because the homeowner moved or changed address), it eventually lands in the state’s unclaimed property database at FLTreasureHunt.gov. One search, one database, covers everything.

The average claim through Florida’s system is $825. In 2024 alone, the state returned $426 million to residents.

England handles council tax through 296 individual billing authorities. Overpayments build up the same way — you move mid-year after paying in advance, your property gets rebanded, or a discount applies retroactively. The difference is what happens next. There’s no centralised database to search. Each council holds its own credits, and if you moved out of that council’s area, they may not have a forwarding address for you.

MoneySavingExpert’s 2024 FOI investigation found that the problem is worst for people who moved between council areas and weren’t paying by direct debit. If you were on direct debit, some councils can refund automatically using your bank details. If you weren’t, your credit just sits there.

Verdict: Florida wins. One centralised database versus chasing individual councils with no single lookup system. England’s approach is fragmented by design, and it shows.

What Happens to Insurance Refunds When You Switch or Sell?

Insurance refunds are one of the messiest categories in both countries, and for surprisingly similar reasons.

In Florida, homeowners insurance is expensive, volatile, and frequently changed. When you cancel a policy mid-term — whether you’re switching carriers, selling the property, or adjusting coverage — the insurer owes you a prorated refund for the unused portion. Straightforward in theory. In practice, the refund often gets routed to your mortgage company or trapped in escrow, then issued later as a cheque to an address you’ve already left.

Florida-specific complications include wind mitigation discount adjustments, retroactive premium changes, and the chaos of hurricane season policy shuffles. Refunds typically range from $50 to $500, but higher premiums (common in Florida) mean higher potential refunds.

In England, buildings insurance works differently but the refund problem is strikingly similar. Switch providers mid-policy, sell a property, or have your mortgage lender arrange new cover, and the old insurer owes you a prorated refund. That refund might go to the mortgage company. The mortgage company might sit on it. Or the insurer sends a cheque to a property you no longer own.

Neither country has a clean mechanism for catching these. No regulator tracks insurance refunds specifically, and they don’t flow into any unclaimed property database in either jurisdiction unless they go uncashed long enough.

Verdict: Draw. Both systems lose insurance refunds the same way — through escrow holdbacks, mortgage company intermediaries, and address changes. Neither side has solved this.

HOA Fees vs Leasehold Service Charges: Where Do Overpayments Vanish?

This is where the comparison gets interesting, because the underlying property structures are fundamentally different — but the financial outcome is the same.

Florida HOAs

Florida has one of the largest HOA and condo association ecosystems in the United States. When you sell a property, prepaid HOA dues, special assessment credits, amenity deposits (pool keys, gate remotes, clubhouse rentals), and transfer fee overpayments can all generate refunds. If your forwarding address is wrong with the association, those cheques bounce around and eventually go unclaimed.

The saving grace is that, eventually, these funds can be reported to the state and appear on FLTreasureHunt.gov.

HOA and Condo Association Overpayments

Florida has a large condo and HOA universe, which means plenty of opportunities for credits to appear. Common HOA and condo refund situations include:

- Prepaid HOA dues when selling

- Special assessment credits or refunds

- Amenity deposits (clubhouse rentals, gate remotes)

- Transfer fee mistakes

- Rare reserve fund credits in unusual circumstances

If you sell and your forwarding address is wrong, HOA-related checks can easily become HOA refund items that you never receive.

With so many potential sources of unclaimed money tied to homeownership, it’s worth doing a comprehensive search. Reclaim Org helps Florida homeowners search for unclaimed funds in one place, making it easier to locate funds linked to old addresses, past lenders, and prior transactions.

England’s Leasehold Service Charges

England’s leasehold system affects almost 5 million homeowners. Leaseholders pay service charges to their freeholder or managing agent for building maintenance, insurance, and communal areas. These charges also include contributions to sinking funds (reserve funds for major works).

The problem? Service charge accounting has historically been opaque. Surpluses from overestimates, credits from cancelled works, and sinking fund adjustments can sit with the managing agent without the leaseholder ever being told.

The Leasehold and Freehold Reform Act 2024 — which received Royal Assent in May 2024 — directly targets this. Key provisions include:

- Standardised service charge demand forms so leaseholders can actually scrutinise what they’re paying

- Mandatory annual reports from freeholders and managing agents

- A ban on opaque buildings insurance commissions, replaced with transparent administration fees

- Removal of the presumption that leaseholders pay the freeholder’s legal costs in disputes

The catch — most of these provisions haven’t come into force yet. The government published a consultation on implementation in July 2025, and secondary legislation is still being drafted. The timeline suggests 2025–2026 for most reforms, but full implementation will take longer.

Verdict: England is behind, but actively reforming. Florida’s HOA overpayments at least have a backstop in the state unclaimed property system. England’s leasehold service charge transparency reforms are in law but not yet operational. Until secondary legislation lands, leaseholders are still dealing with the same opacity they’ve had for decades.

Who Gets Utility Deposit Refunds Back Quicker?

Utility deposits are easy to forget in both countries, and they’re a surprisingly common source of unclaimed money.

Florida homeowners pay deposits when starting electric, gas, water, sewer, cable, and internet service. When you sell and close accounts, final billing credits and deposit refunds get issued. If you’ve already moved and didn’t update your address with every single provider, those cheques — typically $30 to $200 across multiple accounts — never reach you.

There’s no regulated timeline forcing Florida utilities to refund deposits by a specific date. Unclaimed credits eventually get reported to the state, but the lag can be years.

England has a regulatory framework that’s genuinely more protective here. Ofgem’s Guaranteed Standards of Performance set hard deadlines:

- Suppliers must issue a final bill within 6 weeks of account closure

- Credit balances must be refunded within 10 working days of the final bill

- If the supplier misses either deadline, they owe the customer £30 in automatic compensation

That structure matters. According to Energy UK, more than 90% of closed account credit balances are returned automatically. The remaining 10% — about 1.9 million accounts holding £240 million — are mostly cases where the supplier can’t reach the customer because contact details changed.

For homeowners managing utilities during a move, This Old House offers practical guidance on handling utility transitions and energy efficiency that applies regardless of which side of the Atlantic you’re on.

Verdict: England wins. Regulated timelines with automatic compensation penalties give UK energy customers a structural advantage. Florida has no equivalent enforcement mechanism for utility refunds.

Closing Costs and Conveyancing: Different Systems, Same Risk of Forgotten Funds

The mechanics of buying and selling property differ enormously between Florida and England. The financial risk of lost refunds, oddly, doesn’t.

Florida: Title Insurance and Closing Costs

Florida property transactions involve title insurance, recording fees, prepaid escrow items, and various closing costs. Errors and overpayments happen — duplicate title insurance charges during a refinance, overpaid recording fees, unused portions of prepaid items, post-closing lender credit adjustments. Amounts range from $25 to several hundred dollars. Not life-changing individually, but irritating to lose.

England: Conveyancing Holdbacks and Solicitor Retentions

England doesn’t use title insurance the way Florida does. Instead, title risk is managed through the Land Registry system and solicitor-led conveyancing. But solicitors routinely hold retention funds post-completion — money held back to cover potential issues like outstanding search fees, indemnity insurance, or conditions that need to be satisfied after exchange.

Once the retention reason is resolved, that money should come back to you. Sometimes it does. Sometimes it sits with the solicitor’s client account and nobody chases it. Unlike Florida, these funds don’t flow into any central unclaimed property database.

Verdict: Different systems, same outcome. Both jurisdictions create pockets of forgotten money during property transactions. Neither has a strong mechanism for flagging these to the homeowner after the fact.

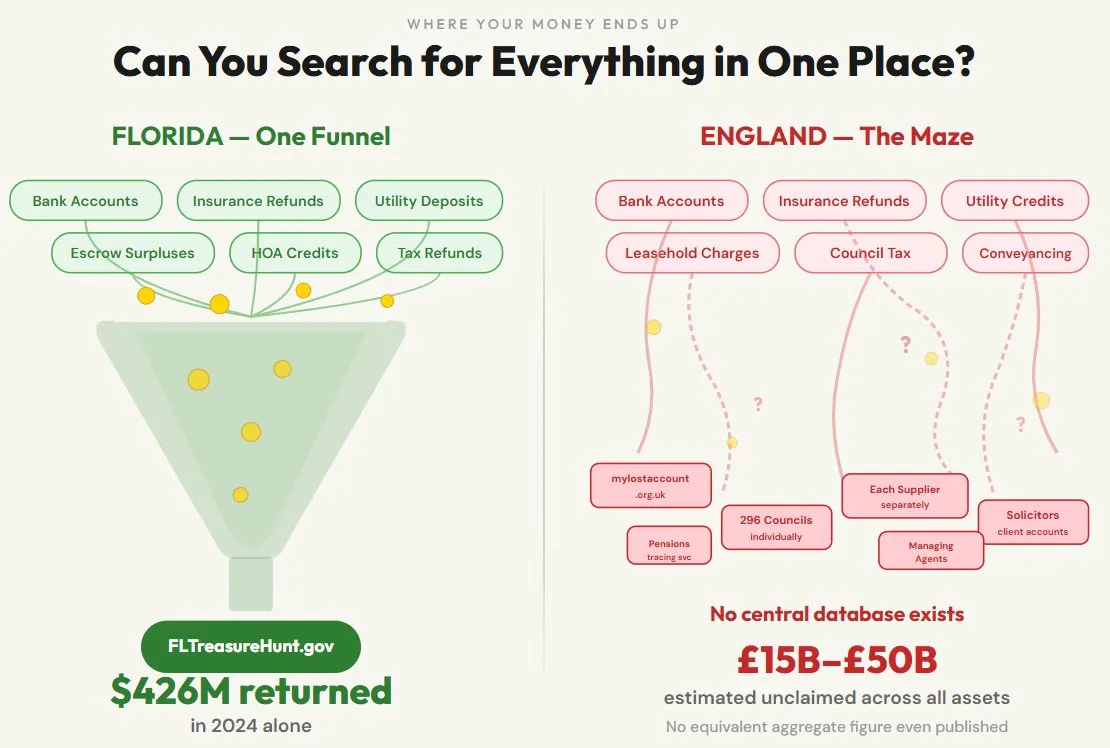

Can You Search for Everything in One Place?

This is where the gap between the two countries is widest.

Florida: One Database

FLTreasureHunt.gov is a single, centralised search that covers all types of unclaimed property — bank accounts, insurance proceeds, utility deposits, escrow surpluses, uncashed cheques, stock dividends, and more. You type your name, search, and see everything the state is holding.

| Florida | England | |

| Central search portal | FLTreasureHunt.gov — covers all property types | No single equivalent |

| Council tax / property tax refunds | Included in central database | Contact each of 296 councils individually |

| Energy / utility credits | Included in central database | Contact each supplier individually |

| Bank accounts | Included in central database | mylostaccount.org.uk (banks and building societies only) |

| Pensions | N/A for this comparison | Pension Tracing Service (separate system) |

| Returned to owners (2024) | $426 million | No equivalent aggregate figure published |

| Total unclaimed | $2.9 billion | Estimates range from £15 billion to £50 billion across all financial assets |

England: Multiple Systems, No Central Hub

England has several search tools, but none of them talk to each other:

- mylostaccount.org.uk — covers lost bank accounts, building society accounts, and NS&I products. Over 70 providers participate. Doesn’t cover council tax, energy, leasehold charges, or anything property-related.

- Individual council websites — for council tax overpayments. Each council has its own process.

- Individual energy suppliers — for closed account credit balances. You need to know who your old supplier was.

- Pension Tracing Service — for lost pensions. Separate system entirely.

The Dormant Assets Scheme, expanded under the Dormant Assets Act 2022, has channelled nearly £892 million from dormant bank accounts to social and environmental causes through Reclaim Fund Ltd. The 2022 Act extended the scheme to insurance, pensions, investment, and securities sectors. But this scheme is about repurposing genuinely unclaimed money for good causes — it’s not a search tool for homeowners looking for their own refunds.

Verdict: Florida wins decisively. A single search that covers everything versus a patchwork of disconnected systems. England’s fragmentation means you need to know where to look before you can start looking — which is exactly the problem when money has gone missing.

A Practical Checklist for Searching in Both Countries

If You Own (or Have Owned) Property in Florida

Gather first:

- All property addresses, including rentals and past homes

- Previous lender and mortgage account details

- Insurance carrier names and policy periods

- HOA or condo association names

- Any previous names (maiden, married)

Then search:

- FLTreasureHunt.gov — search under current and previous names, include former co-owners

- Check each Florida property you’ve owned, not just your current home

- Look back 5–10 years; many refunds surface well after the triggering event

- Search annually, especially after refinancing or selling

If You Own (or Have Owned) Property in England

Gather first:

- All property addresses, including any buy-to-let or previously owned homes

- Names of previous councils (for council tax)

- Previous energy suppliers and account numbers if you have them

- Solicitor details from past purchases or sales

- Managing agent or freeholder details (for leasehold properties)

Then search:

- Your old council — search “[council name] council tax refund form” online, or ring them directly

- Your old energy suppliers — log into old online accounts if possible, or call. Ofgem’s recent campaign specifically targets the £240 million sitting in closed accounts

- mylostaccount.org.uk — for any lost bank or savings accounts

- Your solicitor — ask whether any retention funds from past transactions are still held

- Your managing agent — request a full service charge statement to check for credits

Make this an annual habit. Both countries add new unclaimed funds to their systems continuously.

The Short Version

Florida and England share the same fundamental problem — homeownership creates a long chain of financial transactions, and at every link, small refunds and credits can fall through. The difference is infrastructure. Florida built a single centralised system that catches most of it. England relies on homeowners knowing exactly where to look across a fragmented landscape of councils, suppliers, and regulators.

On utilities, England’s Ofgem rules are genuinely better — regulated timelines and automatic compensation give homeowners a structural advantage Florida doesn’t match. On everything else, Florida’s centralised approach is harder to beat.

Either way, the money exists. Checking takes minutes. And most people who search find something they didn’t know was there.

References

- Florida Department of Financial Services — Division of Unclaimed Property: FLTreasureHunt.gov

- CFO Jimmy Patronis press release, January 2025 — $426 million returned in 2024

- MoneySavingExpert — Council tax overpayments investigation (FOI data, March 2024)

- MoneySavingExpert — How to reclaim overpaid council tax

- Ofgem — £240 million in closed energy account balances (October 2025)

- Ofgem — Guaranteed Standards of Performance and automatic compensation rules

- Energy UK — Customer credit balances explainer (March 2024): energy-uk.org.uk

- Leasehold and Freehold Reform Act 2024 — Royal Assent May 2024, implementation timeline: commonslibrary.parliament.uk

- GOV.UK — Strengthening leaseholder protections consultation (July 2025): gov.uk

- GOV.UK — Dormant Assets Scheme strategy and £892 million released: gov.uk

- Dormant Assets Act 2022 — legislation: legislation.gov.uk

- My Lost Account — free UK bank account tracing service: mylostaccount.org.uk

- Florida Statute § 627.4133 — Cancellation and nonrenewal of homeowners insurance policies: flsenate.gov

- GOV.UK — Council tax levels in England 2024–2025: gov.uk